top of page

Find new business opportunities designing products that contribute to solving planetary problems

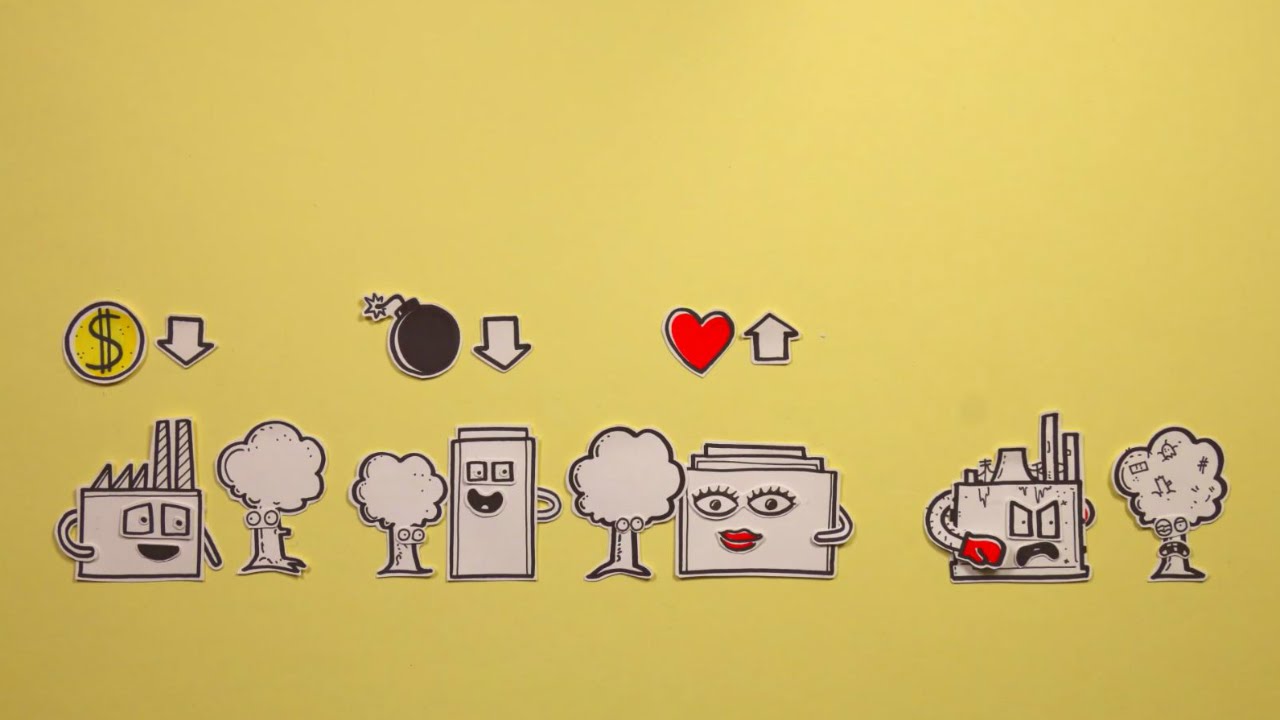

Move from business as usual to

TRUE BUSINESS SUSTAINABILITY

Upgrade business sustainability efforts to become a true force for good

bottom of page